Entities endorsed as deductible gift recipients (DGR) are entitled to receive donations which are deductible from the donor’s income tax. Division 30 of the Income Tax Assessment Act 1997 determines which entities can gain DGR status.

There are two types of DGR:

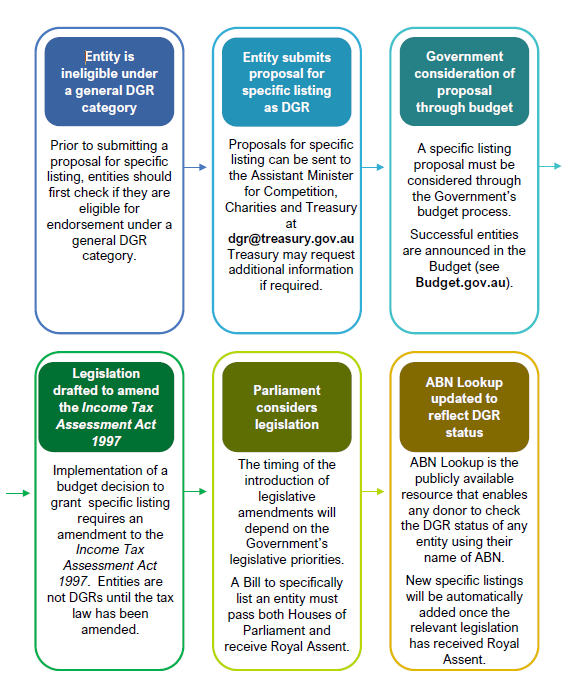

An entity may gain DGR status by applying for endorsement under one of 52 DGR endorsement categories. Eligibility under those categories is based on the entity’s purpose or the purpose of a fund, authority or institution it operates. The Australian Taxation Office website provides information about the eligibility for endorsement under DGR categories.

There are two ways to apply for DGR endorsement with the Australian Taxation Office:

Not-for-profits can seek guidance on DGR categories and how to apply for DGR endorsement by contacting the Australian Taxation Office Not-for-profit advice service on 1300 130 248 Monday to Friday, 8 am to 6 pm AEDT. Entities can also email atoendorsements@ato.gov.au.

If an entity does not fit into the existing DGR categories, an entity may submit a proposal to be specifically listed by name in the tax law.

Specific listing is intended to be used only by exception. Of around 29,000 entities with DGR status, only around 230 are specifically listed.

Specific listing of an individual entity involves consideration by the government through the budget process, followed by consideration by the Parliament through an amendment to the tax law. Proposals are assessed against a range of factors, including the unique characteristics of the entity and the broad public benefit.

Proposals to specifically list an entity should be submitted in writing to the Assistant Minister for Competition, Charities and Treasury, via dgr@treasury.gov.au.

Each proposal is a policy proposal that is considered by government through the budget process. To ensure your proposal can be costed, your written submission must include:

| Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | |

|---|---|---|---|---|---|

| Individuals | - | - | - | - | - |

| Business | - | - | - | - | - |

| Ancillary Funds | - | - | - | - | - |

Other factors that you may wish to address to support your proposal include:

Proposals for specific listing are considered by government through the budget process, so submitting a proposal at least six months in advance of the annual Budget or Mid-Year Economic and Fiscal Outlook update is recommended.

Proposals that are agreed by government will be announced as part of the regular budget updates (see Budget website for timing and access to current and past budget documents).

Specific listings proposals are then considered by Parliament through a Bill that proposes amendments to the tax law. The timing for introduction of tax law amendments is at the discretion of government. The government will typically not include an entity in a Bill until any outstanding conditions have been met and the entity’s governing documents contain appropriate public fund rules.

A Bill that is passed by Parliament must receive Royal Assent before it comes into effect as an Act. The Act will specify a commencement date – this is the date of effect for DGR status.

If your entity’s proposal is not announced by the government in the relevant budget update, you can submit a new proposal at any time.

A DGR specific listing is a not an administrative decision, but a legislative matter that requires an Act of Parliament. Merit review is not available.

The specific listing of an entity may be subject to a limited time period, which is specified in the tax law (see Income Tax Assessment Act 1997). At the end of the legislated time period, an organisation’s specific listing will sunset.

Any entity can propose an extension of their specific listing period. A proposal for an extension of the time period is considered through the same process as any other specific listing proposal. The proposal must be considered through the budget process by government and then considered by Parliament through amendments to the tax law. To facilitate this, entities seeking an extension must follow the How to submit a proposal for specific listing above. Entities are encouraged to make a proposal for an extension in advance of the sunset date.